New York Market Summary: 2026 Q1’

Winter after the holidays can be a strange time of year. The streets are cold, and the margins are thin. Not a lot of movement until tax season. The perfect chance to do a sanity check—before the Spring bells ring and you’re forced to choose: go in with a plan or bite down and swing for the fences.

Head Count

Since 2024, New York’s adult-use program has continued its steady expansion, not a stampede, not a stall.

2024: 1,977 total licenses

2025: 2,201 total licenses

2026: 2,665 total licenses

New York State Licenses

That’s a +35% increase since 2024 and +21% year-over-year into 2026.

License types seeing the most growth:

Retail Dispensary Licenses: 503 → 516 → 569

Cultivator Licenses: 251 → 256 → 315

Microbusinesses: 321 → 372 → 438

Processor Licenses: 332 → 377 → 423

Licenses by City

Density Study

By 2026, licenses remain heavily concentrated where foot traffic and demand justify the overhead:

License Count by City

Brooklyn (153) and New York City proper (142) continue to dominate.

Buffalo, Rochester, and the Bronx form a second tier—meaningful counts, but more controlled.

Smaller markets (Albany, Yonkers, Newburgh, Ithaca, Kingston) show modest growth, not overreach.

The pattern is consistent: urban cores absorb licenses first, secondary cities follow cautiously, and smaller markets avoid overexposure. No one’s stacking plants where the soil can’t support it.

Retail Report

Out of 576 approved retail licenses listed by OCM, 360 have been verified through Google business data, 173 maintain active online menus

That gives us:

62.5% coverage of operating retail locations

30.0% menu-level visibility

For NY city, we got 66 active menus giving us 34,000+ lines of product data

This is not full market coverage—but it’s enough to do a sniff test.

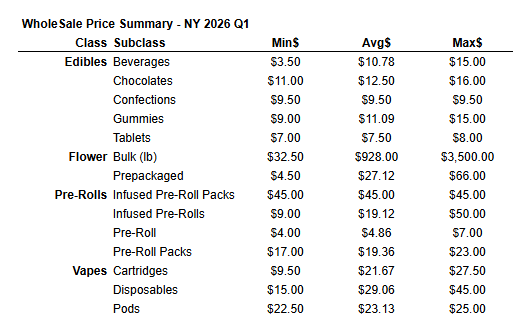

Edibles

Edibles show the cleanest pricing structure in the dataset—tight ranges, low volatility, very little experimentation.

Beverages: $3.50 → $10.78 → $15.00

Entry-friendly, impulse-ready, consistent margin plays.Chocolates: $11.00 → $12.50 → $16.00

Premium positioning, but not drifting into novelty pricing.Confections: Flat at $9.50 across the board.

That’s not an accident—that’s buyers enforcing discipline.Gummies: $9.00 → $11.09 → $15.00

Still the workhorse. Still the safest bet.Tablets: $7.00 → $7.50 → $8.00

Niche, functional, and priced accordingly.

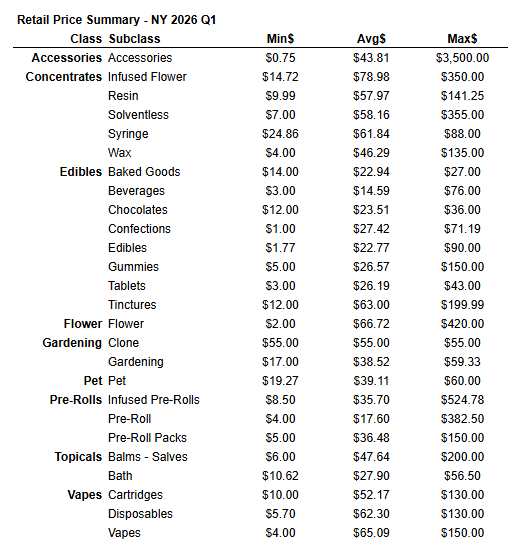

Retail (Avg):

Gummies: $26.57

Chocolates: $23.51

Beverages: $14.59

Tablets / Confections / Baked Goods: ~$22–27

Spread: ~2.0x–2.5x

Edibles is the most mature category, aligned with CPG structure.

Flower: A Market Split in Plain Sight

This is where things get loud.

Bulk Flower (lb): $32.50 → $928.00 → $3,500.00

That range tells you everything you need to know. New York isn’t one flower market—it’s several stacked on top of each other. Outdoor, greenhouse, indoor, Trim…

Prepackaged Flower: $4.50 → $27.12 → $66.00

Retail (Avg):

Flower (general): $66.72

Max retail hitting $420, but that’s not the median story.

Spread: Massive—but intentional.

Pre-Rolls: Volume First, Novelty Second

Standard Pre-Rolls: $4.00 → $4.86 → $7.00

That’s a volume product. Plain and simple.

Infused Pre-Rolls: $9.00 → $19.12 → $50.00

A wide spread, but buyers are selective—most action sits in the middle, not the flex tier.Infused Pre-Roll Packs: Flat at $45.00

Retailers want predictability here. No surprises.Pre-Roll Packs (non-infused): $17.00 → $19.36 → $23.00

Retail (Avg):

Pre-Rolls: $17.60

Infused Pre-Rolls: $35.70

Pre-Roll Packs: $36.48

Spread:

Standard: ~3.5x

Infused: ~1.8x–2.0x

Standard pre-rolls are treated like trim runs—high turnover, low romance. Infused options are where retailers slow down, explain, and upsell.

Vapes: Where Buyers Are Still Willing to Pay

Cartridges: $9.50 → $21.67 → $27.50

Disposables: $15.00 → $29.06 → $45.00

Pods: $22.50 → $23.13 → $25.00

Retail (Avg):

Cartridges: $52.17

Disposables: $62.30

Vapes (general): $65.09

Spread: ~2.2x–2.5x

This is the cleanest markup story in the market. Hardware plus oil still sells, still commands trust, and still justifies price. Retailers aren’t apologizing for vape pricing—and customers aren’t pushing back hard enough to change it.

Concentrates: Retailers Are Still Defending This Category

Wholesale (Avg):

Resin / Solventless: ~$58

Wax: ~$46

Retail (Avg):

Resin: $57.97

Solventless: $58.16

Wax: $46.29

Infused Flower (concentrate-adjacent): $78.98

Yes—some averages look flat because the dataset includes aggressive promotions and legacy carryover pricing

One of the most obvious insights from this dataset is New York’s upper-tier product pricing is significantly higher than in many other adult-use markets—especially more than New Mexico.

Example:

Xiaolin (NY): $300 to $500 depending on weight/size.

Goliath (NM): Micro-producer tier, a modest $30

Even without a name brand to compare to. New York supports ultra-premium offerings in ways smaller or price-sensitive markets like New Mexico can't—or won’t.

Once you enter the entry-level tier, brand loyalty disappears.

It doesn’t matter who made the gram pre-roll if it’s the cheapest on the menu. Scraping thousands of SKUs showed this pattern clearly:

Consumers care about price, not branding, when they’re bargain hunting.

So what matters?

Lowest option

Mid-range average

Highest priced item

You don’t need to know every brand—just how they’re priced, and whether your product needs to undercut or simply coexist.

Takeaway: For competitors, don’t get distracted by who’s on the menu. Get focused on where your product lands on the price ladder.

Dutchie Controls the E-Commerce Flow

In terms of visibility and online retail infrastructure:

Dutchie dominates the e-comm stack in New York.

Leafly and Weedmaps have minor placement compared to what we’ve seen in other markets.

Surfside.io is already integrated with NY menus, acting as a browser overlay for shopper behavior and marketing targeting.

This is big. It shows that even at this early stage of retail expansion, ancillary tech platforms have already set up shop, and operators are beginning to rely on them for digital strategy.

Pricing Intelligence > Brand Inventory

One of the most important operational takeaways:

You don’t need to catalog every brand.

You need to:

Spot the low, mid, and high tier SKUs

Understand where your brand or client will land

Decide: compete, undercut, or differentiate

This isn't a beauty contest—it’s a pricing war dressed up as a menu. Focus on your numbers and getting shelves full before investing in one of every product.